America's Grid Battery Boom is Just Getting Started

2024 was a record-breaking year for grid batteries in the US. This year developers plan to build even more storage capacity.

A quick editor’s note: Before getting into our regularly scheduled newslettering for the week, I wanted to share a new free clean energy tracking tool that I recently built. Using Cleanview’s data—and a lot of help from my programming guru Claude—I created clean energy project dashboards for every state and clean energy technology in the U.S.

With these dashboards, you can easily view the largest and most recently built solar, wind, and battery projects in every state. And because everyone loves a good map, you can view them all on a map too. Check them out by clicking the links below:

My hope is that these free tools will be helpful to everyone from clean energy professionals to activists to climate journalists. If you have any questions or feedback on how they can be improved, send me a note at michael (at) cleanview.co

Alright onto the main story!

Battery storage goes mainstream

In the last newsletter, I shared some highlights from Cleanview's 2025 State of Clean Energy Deployment report, focusing on the remarkable growth of solar in 2024. Today, I want to dive deeper into what might be the most exciting story from our research: the explosive growth of battery storage.

While solar continues to dominate clean energy headlines (and rightfully so), battery storage has quietly transformed from a niche technology into a mainstream grid resource. The numbers we uncovered in our analysis paint a picture of an industry hitting its stride at precisely the moment when the grid needs it most.

What makes the battery storage story particularly compelling is how quickly the technology has matured. Just five years ago, utility-scale batteries were still considered experimental by many grid operators and utilities. Today, they're being deployed at gigawatt scale and playing crucial roles in maintaining grid reliability during extreme weather events, reducing electricity costs, and enabling higher penetrations of renewable energy.

Below, I'll share some of the key findings from Cleanview’s report about battery storage. If you missed our previous newsletter on solar deployment or want to read the full report, you can find those here and here.

Now, let's get into the data and see what it tells us about battery storage's breakout year.

Battery storage growth accelerated in 2024

The U.S. added 10.9 GW of utility-scale storage capacity in 2024, a remarkable 65% increase compared to 2023’s storage additions.

At this point, many of us are used to hearing about record years in clean energy deployment. What makes 2024’s storage growth so impressive is that it represents an acceleration from the previous year's already substantial growth rate (65% vs. 56% in 2023).

California and Texas continue to lead

While battery storage deployment is growing across the country, two states continue to dominate the landscape. California and Texas accounted for 60% of all new storage capacity built in 2024, a continuation of a trend that has played out over the last few years.

California maintained its leadership position, adding 3,152 MW (11,237 MWh) of new capacity in 2024. The Golden State's early policy support for storage, its high electricity prices, and aggressive clean energy goals have made it a natural incubator for battery projects. (I wrote more about California’s early storage policies here).

Texas, meanwhile, built 2,832 MW (4,536 MWh) of new storage capacity. What's notable is that Texas achieved this growth without the same policy mandates as California. Instead, the state's fast-to-connect interconnection processes, volatile electricity prices, and high demand growth have created strong incentives for storage deployment.

New leaders emerge in the West

One of the most significant developments of 2024 was the emergence of several Western states as significant players in the battery storage market.

Arizona vaulted into third place nationally by adding 976 MW of capacity, bringing their total capacity to 2,120 MW. Unlike other states, Arizona has focused on longer-duration storage projects lasting about 4 hours on average vs. 1 or 2 in other states. That helped the state add 4 GWh of energy capacity in 2024.

Nevada also saw explosive growth, doubling its storage capacity by adding 565 MW in 2024. The state's solar resources, growing population (and load), and proximity to California markets have made it an attractive location for developers.

Hawaii (73 MW, 20% growth), New Mexico (150 MW, 63% growth), and Colorado (78 MW, 47% growth) all expanded their storage capacity significantly, though at more modest scales than the market leaders. In each of these states fossil fuel retirements and aggressive clean energy policies are driving growth.

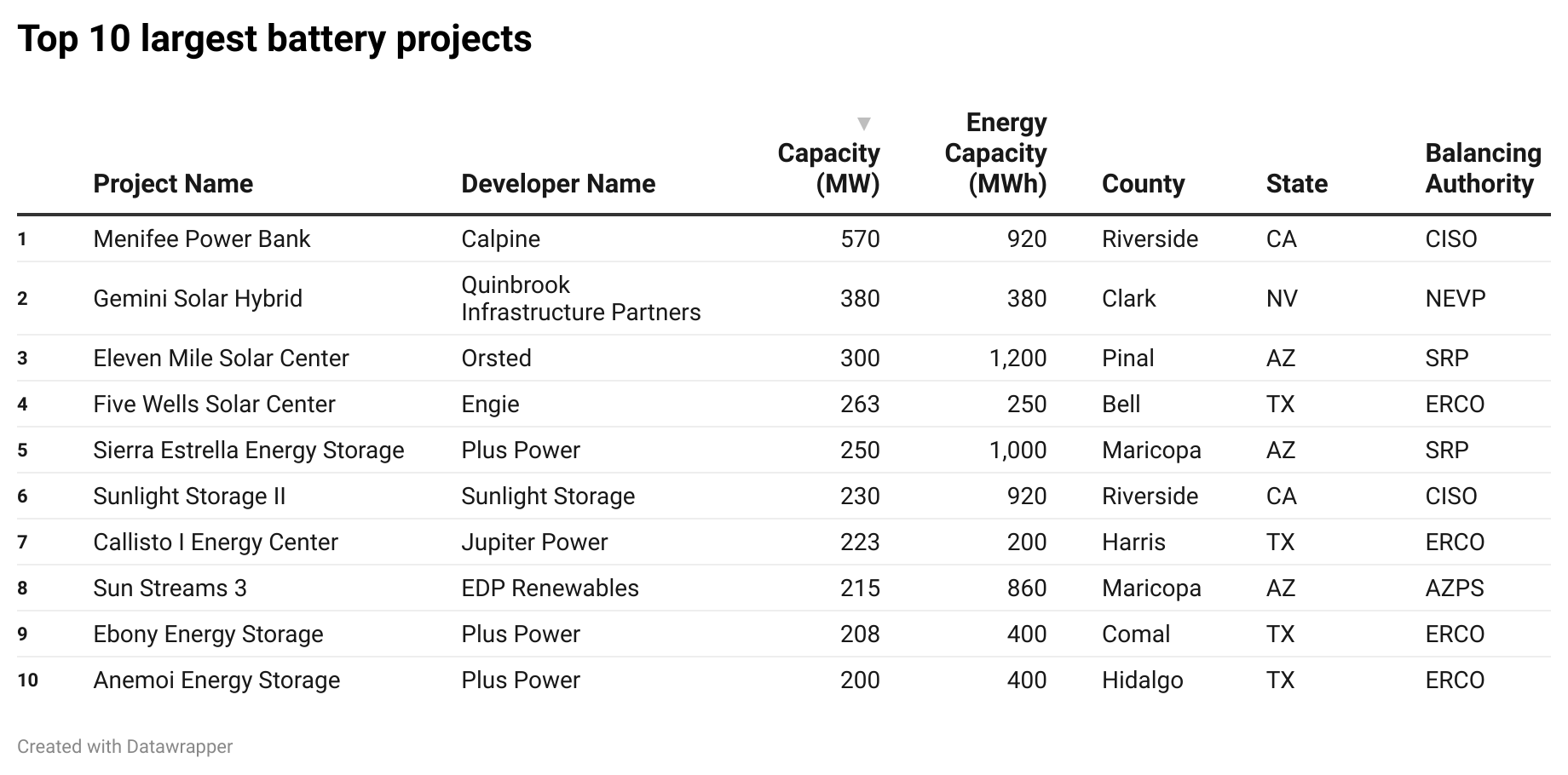

Mega storage projects

Just as we've seen with solar, the scale of individual battery projects continues to grow each year. The largest project brought online in 2024 was Calpine's Menifee Power Bank in California's Riverside County, with 570 MW of capacity and 920 MWh of energy storage.

The second-largest project was built at Nevada's Gemini Solar facility, where Quinbrook Infrastructure Partners added 380 MW of storage capacity, creating one of the nation's largest solar-plus-storage hybrids.

Project economics and the benefits of scale are the primary drivers of this megaproject trend in battery storage. As I wrote last year, it’s significantly cheaper to build a megaproject than it is to build a small storage facility on a per MW or MWh basis.

Top developers built 33% of storage capacity

As is the case in the solar and wind development world, battery storage development is fairly concentrated. The top 10 developers built 33% of all new storage capacity in 2024.

Plus Power led the pack (no pun intended) with 748 MW of capacity spread across 4 projects. Calpine came in second with 658 MW of capacity, but led in terms of energy capacity (MWh), building a total of 2,522 MWh across 6 projects.

The road ahead for batteries in America

As I wrote in the last newsletter, there’s much uncertainty ahead for clean energy.

Republicans in Congress recently passed a resolution instructing their members to identify $2 trillion in spending cuts over the next 10 years to pay for President Trump’s huge tax cuts. House Speaker Mike Johnson has made it clear that many of the policies and incentives in the Inflation Reduction Act (IRA) are on the chopping block. Which of these incentives will be cut remains to be seen.

But most of these impacts will be felt after 2025. Much of the growth in energy storage has been driven by the 30-50% investment tax credit (ITC) incentive available for standalone and paired hybrid projects. Those are locked into the tax code for 2025.

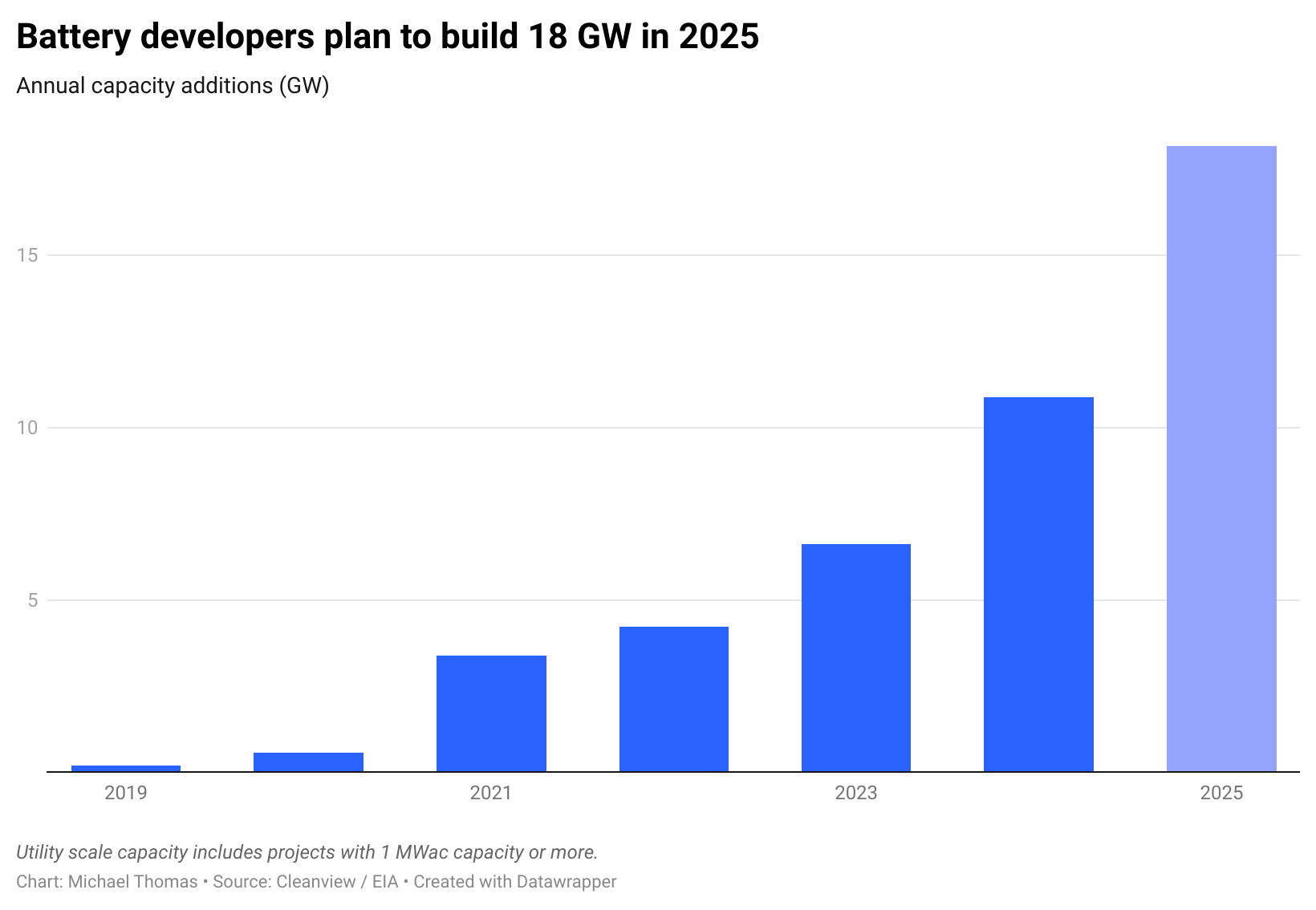

Even with Trump in the White House and Republicans in charge of both branches of Congress, storage is on track for another record-breaking year in 2025. Developers expect to build 18.1 GW of new capacity – nearly double what was built in 2024. Of that total, 12.3 GW is already under construction or awaiting final commercial operation.

If these projections hold, we would see capacity growth of 68% in 2025, an even faster pace than 2024’s record-setting year.

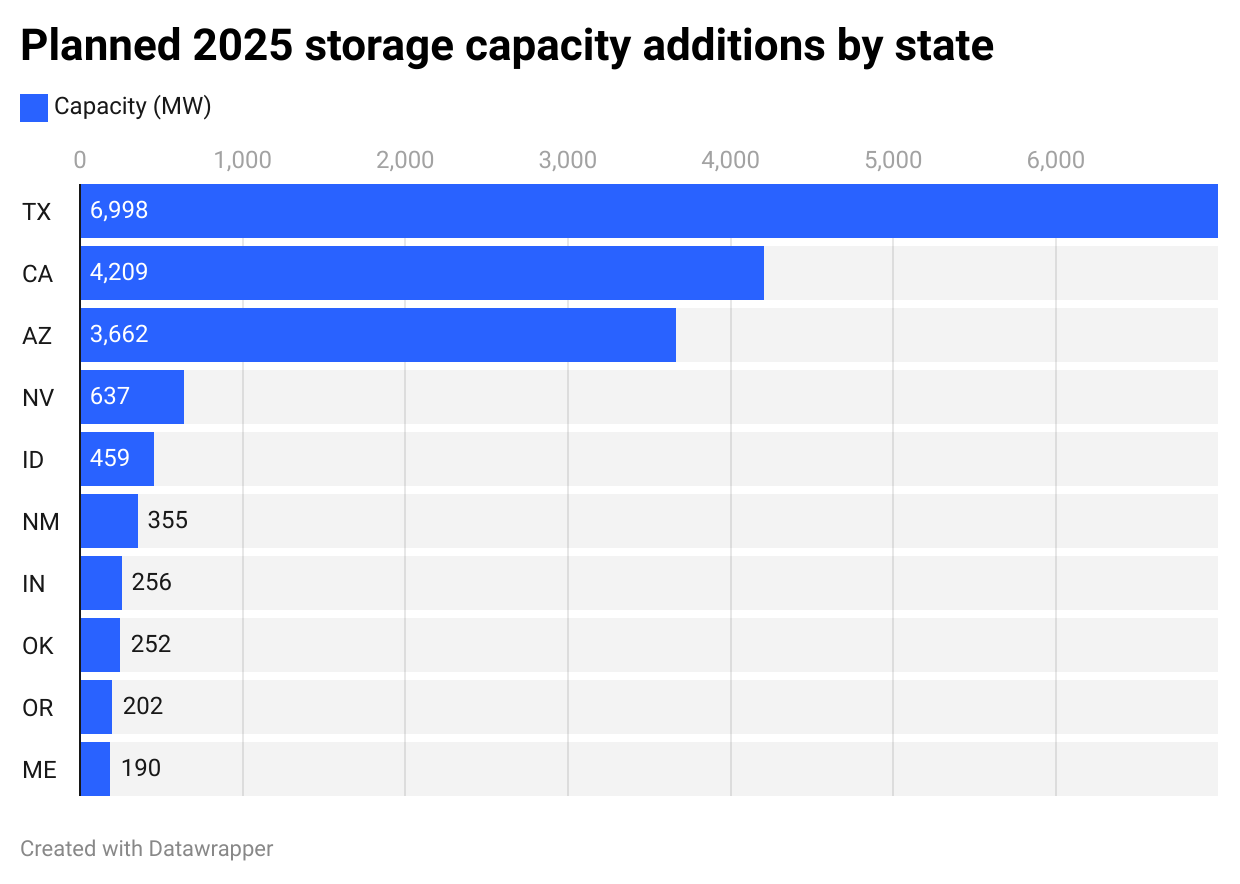

Perhaps most significantly, we're about to witness a changing of the guard in storage market leadership. Texas is projected to overtake California as the #1 storage market, with developers in the Lone Star State planning to build 7 GW of new capacity in 2025 – a 54% increase from their 2024 total.

California isn't slowing down either though, with plans for 4.2 GW of new storage in 2025 (34% growth). Arizona is also expecting explosive growth, with storage additions potentially increasing by 375% to reach 3.7 GW.

The scale of individual projects is also set to increase further in 2025. The pipeline includes multiple 500 MW facilities, such as Avantus's Bellefield Solar and Storage Farm in California and Hecate Energy's Ramsey Storage in Texas, along with numerous 400 MW projects across different states.

What we're witnessing with battery storage is reminiscent of solar's trajectory a decade ago—a technology moving from the margins to the mainstream at breathtaking speed.

Track clean energy projects across the country

Cleanview tracks thousands of clean energy projects across the country at every stage from permitting to final construction. To learn more sign up for a demo of the platform below.

Or check out our free datasets and tools below:

Very hopeful to see this expansion. Spread the good word!

So what does all of this mean in terms of reductions of CO2 and greenhouse gas emissions? I’m curious to know if you cover that aspect. Reason being is with data centers on the rise and a corresponding increase in CO2 emissions in particular and GHG emissions in general, what it sounds like to me is with all this storage capacity, such could potentially (or maybe does) offset the data centers-driven CO2 and GHG-emissions increase. As best I can recall, I haven’t seen where anyone is correlating the two and putting this down in writing.