The New IRS Clean Energy Tax Credit Rules, Explained

I asked Clean Energy Counsel's Zach Crowley to explain the Treasury Department's "begun construction" guidance to me.

For the last week, I’ve been trying to wrap my head around the Treasury Department’s new clean energy tax credit guidance, or “begun construction” rules. When the new rules were released last Friday, my initial reaction was that the rules were a disaster for clean energy.

When I published that assessment, I received a lot of messages from respected developers and analysts arguing that I was too pessimistic. (I summarized and published the feedback I received here).

It turns out clean energy tax rules are complicated! So for that reason, I reached out to an expert in the field to ask him to explain the new IRS ruling to me and answer my questions.

Zach Crowley is a Partner at the law firm Clean Energy Counsel. His speciality at the firm is all things tax credits, so he knows more than just about anyone about this stuff. Here’s a transcript of our conversation:

What are the major changes to the rules folks should know about?

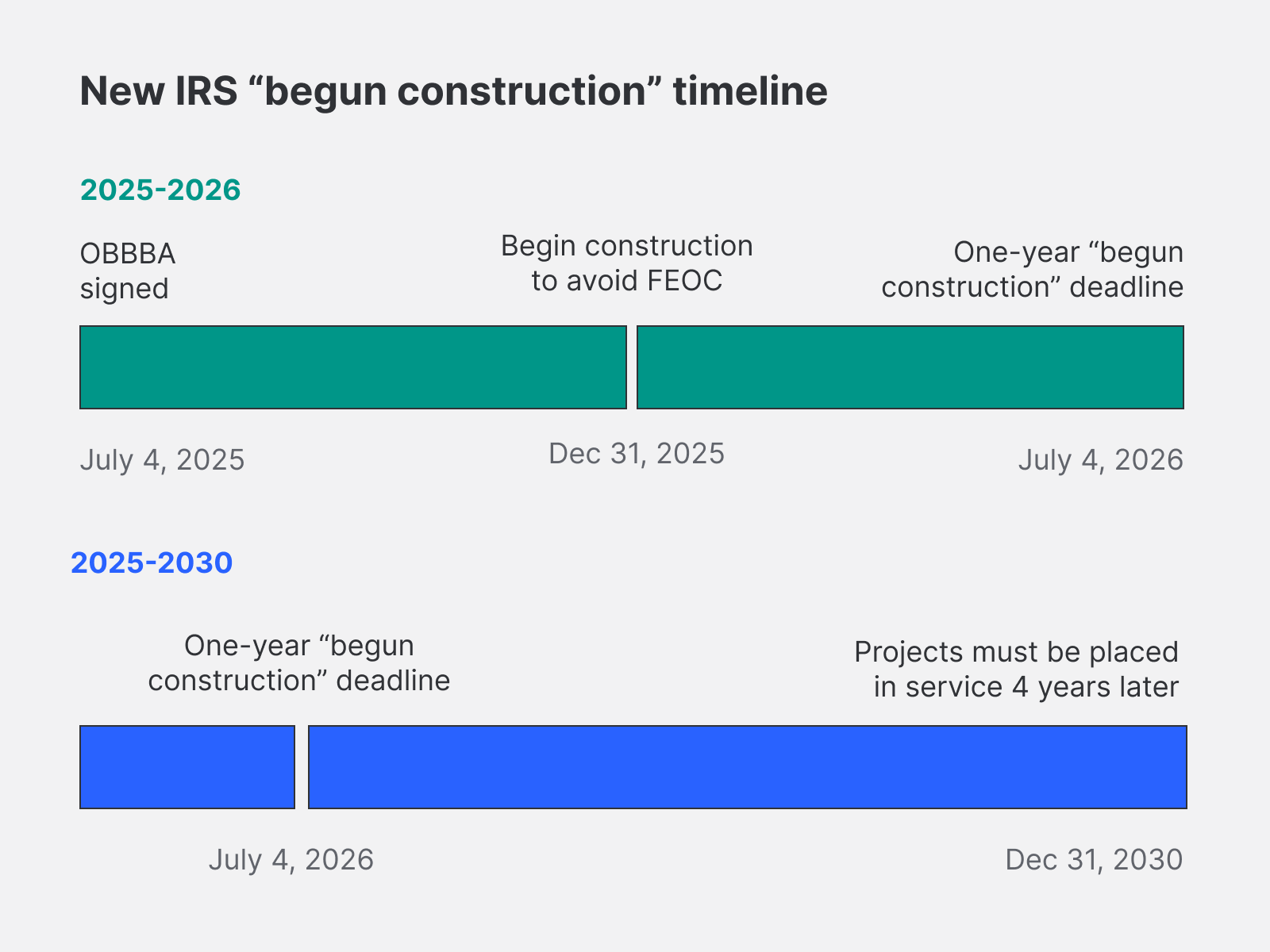

The big change is that on September 2nd the 5% safe harbor is no longer available for projects unless they are under 1.5 MW in size.

The physical work test remains. You can continue to begin construction until July 4th of 2026 in order to retain four years of continuity. It also—just like the prior guidance—clarifies that if you are outside of that four years of continuity that you have a facts and circumstances test to show the physical work.

There are some changes from the prior begun construction guidance. An example of that is previously the facts and circumstances tests outside of that four years were a little bit easier to satisfy. There were things like getting permits, entering into other contracts. These examples would have been clear evidence of you continuing that work for the continuity. Now there's a requirement for on-site construction continuing to occur. So if you're not within that four-year safe harbor window, there's going to be more qualification that you need to show evidence of the work that you are doing on an ongoing basis to satisfy that test.

Physical work can be on-site or off-site. Can you explain the difference?

For on-site work, the specific notice includes an example of installing racking, scaffolding, excavating foundations. Historically we've seen other folks use the building of roads that are necessary for the project itself as long as they're substantial. I think pouring concrete, things like that, are all good evidence.

In terms of tips, you need to document everything. What's really necessary for most financing parties is some kind of report, ideally by a third party where someone comes on site and they say here are all the physical examples of on-site work that's occurred. Ideally you don't leave it to a single action. It's better to say here I'm building a road, and I've poured concrete, and I've installed some of the racking.

Off-site is generally the ordering of customized equipment. Mostly it's limited to things like transformers, inverters, power conditioning equipment. We have seen other folks look at this for racking.

You need to enter into a binding written contract to build that on your behalf. Then there are specific rules about what can be included in the contract including the amounts of damages that can be paid as a result of non-compliance.

So for that off-site work, there’s no spend requirement, right?

That's right. It does not say that you have to spend $100,000. What you do need is a binding contract. When we say a binding written contract, what it means is that you will have to pay. There will be damages if you do not pay.

In general, you need to be above 5% if there's going to be a liquidated damages termination provision. Liquidated damages are circumstances where, as a result of a termination, there's just an automatic payment. Really what they're looking for is skin in the game.

I’ve heard it’s cheaper to do that off-site work than use the 5% safe harbor. Is that true?

It's dependent on each individual project but it is generally less than the 5%.

Some folks have entered into contracts for customized subcomponents of those major components like inverters or transformers. And by entering into the beginning stages of building that customized equipment they've said that's the beginning of construction. Those might cost hundreds of thousands of dollars relative to a $100 million project.

The issue is that if I'm a tax equity investor, I have to get comfortable with this. There always a balancing of what people describe as a sniff test. Like is it really going to be reasonable to go to the IRS and say I incurred $10,000 on a $200 million project and that should be enough to show that I did physical work?

The other point is that most of those kinds of equipment are long lead time items. Transformers are long lead time in terms of how long it takes to build them. [Editor’s note: That means you don’t have to pay 100% immediately upon signing the contract].

How will this impact projects that get delayed due to permitting?

Let's say that a project orders transformers and satisfied the requirements for physical work. They then have four years to place the project in service. If they do that this year in 2025, it would be the end of 2029. That gives them time to get the permits that they need.

But in a circumstance where they did not get the permits that they needed, they could still satisfy the continuity of that continuous construction, if the reason for the delays were, as an example, certain delays on permitting. But in that situation, they're in that facts and circumstances test. They're outside of the four-year continuity safe harbor.

So, what it means is when they go to file returns, there could be an audit that the IRS would say, well, we're looking at what you did over the course of the, let's say, five years, and it was not sufficient for showing an ongoing physical work of significant nature.

So, I think it's certainly possible that if you didn't get one of those permits and it’s delayed and delayed and delayed, it's going to be very difficult to show your satisfaction of those facts and circumstances even with that delay because you're just not able to do anything on-site during that time.

So in that case you might struggle to find a tax equity investor comfortable with taking that risk, right?

That's right. Historically, most investors and lenders have been really focused on the safe harbor period. Certain projects took four, five or six years. It was possible for those projects to satisfy the facts and circumstances test, but it's always been really difficult to get those funded.

I think a big question of whether you will be able to get those funded when that happens is what does the political landscape look like at that point? Because that’s in 2029 or 2030. Who's at Treasury? Who's the IRS?

I think that it's going to be difficult for projects with long permitting delays. But not just because of the issue around your eligibility for tax credits. Because power purchase agreements and site control and every other material project contract usually has time frames under which projects need to be built. So there are huge cascade of effects that end up happening when there are those big delays.

Are there other timelines people should be thinking about?

The obvious one is July of next year. If you don't begin construction by then, it's going to be hugely difficult.

But that's not true for smaller projects, right? With the timelines for residential, small commercial, industrial projects, you could begin construction after July of 2026 and put a project in service within a year or something [which is before the December 31, 2027 deadline].

Zach Crowley is a Partner at the law firm Clean Energy Counsel. You can read the firm’s summary of the new IRS guidance here and sign up for an upcoming webinar with more on the new rules here.